Your trusted adviser for R&D Tax Credits, Creative Tax Relief, and R&D Grants

Your trusted adviser for R&D Tax Credits, Creative Tax Relief, and R&D Grants

Your trusted adviser for R&D Tax Credits, Creative Tax Relief, and R&D Grants

Your trusted adviser for R&D Tax Credits, Creative Tax Relief, and R&D Grants

The Video Games Expenditure Credit (VGEC) is a government funding incentive that allows digital game producers to claim 34% of their core production expenditure as a tax credit. It replaces the Video Games Tax Relief scheme.

The Video Games Expenditure Credit (VGEC) is a tax credit incentive designed to support UK-based game developers. VGEC can be claimed on qualifying expenditure incurred from 1 January 2024.

Video Game Development Companies (VGDCs) can claim up to 80% of their UK development costs at the end of their accounting period and receive either a cash credit or money off their tax bill.

It replaces the previous incentive, Video Games Tax Relief (VGTR); this scheme remains open until 31 March 2027 for companies who begin production on their game before 1 April 2025 (and until 31 March 2025 for those who do not).

Development companies can claim back 34% of their UK-based core costs as an above-the-line credit.

Eligible companies can claim the lower of:

The credit will be treated as income and is taxable at the Corporation Tax rate of 25%. Therefore, the real-world benefit is 25.5% of the qualifying expenditure!

VGDCs can receive their expenditure credit as a deduction of their tax bill or as a cash credit.

If you are a UK-registered company and have been developing your own video game, then you will likely qualify for VGEC.

Your company must be responsible for the designing, developing, testing, and production of the video game and, therefore, be known as the Video Games Development Company (VGDC).

If two or more companies are working on the same game, only one can apply for VGEC.

A VGDC doesn’t need to take direct responsibility for every aspect of developing the video game, but must have overall accountability for the game.

Video games are eligible, no matter what device they can be played on. Games played on PCs, smartphones, tablets, and video consoles are all potentially qualifying.

However, games designed for advertising purposes, gambling or with extreme material cannot be claimed.

Qualifying games must be intended for the general public and must be certified as "British" by the British Film Institute by passing the Cultural Test.

VGDCs also need to spend at least 10% of ‘core costs’ of development within the UK to claim for a game.

The Video Games Expenditure Credit is claimed as part of the Company Tax Return (CT600) filed with HMRC. To make a VGEC claim, you’ll need to be registered as a company and have the following documents:

The VGEC is treated as taxable income and thus is taxed at the main Corporation Tax rate (25%).

It must first be used to pay off your Corporation Tax liability; any leftover can be used to pay off other liabilities or claimed as a cash credit.

"DR Studios, part of the 505 Group, has worked closely with Myriad since 2018, particularly with Chris Dowsett, who has managed several BFI (British Film Institute) certification applications and subsequent video game tax relief (VGTR) claims for us. Chris is an excellent 'details' man. He's managed both our BFI certification applications and subsequent tax relief claims from start to submission, and we couldn't be happier with the relationship. Chris is backed by the specialist tax team at Myriad, which has years of experience in the creative industry tax relief field. I recommend Chris and Myriad if you're considering a VGTR claim."

Andrew Stephens

DR Studios - Part of 505 Group

"I've worked with Chris Dowsett at Myriad since 2017, identifying qualifying R&D criteria while navigating BFI & HMRC submissions. Chris' knowledge of the entire VGTR process has exceeded my expectations and placed my business in a stronger position. I highly recommend Chris to all my business friends and connections."

Paul Adams

Full Fat Productions

"Chris at Myriad has greatly supported Teach Your Monster over the last five years, working with us to manage our annual VGTR claim for multiple games. His process knowledge is quite remarkable, given the detail and complexity involved. We have a high level of comfort knowing our claims are worked through with great attention to detail and with every area thoroughly scrutinised before submission. This has resulted in significant financial benefits to support our ongoing work developing educational kid's games. Chris is very approachable, always there when you need him, he knows his stuff inside out, and last but not least, he is very pleasant to work with!"

Alison Duddy

Teach Your Monster

"Chris and the team at Myriad did a fantastic job with our VGTR claim. They were fast, supportive and knowledgeable. I would highly recommend."

Martyn Johnston

Upperroom Games

In our latest VGEC eBook, we explain how you can make the most of this valuable government programme.

Our guide will take you through all the steps required to complete and pass the BFI's Cultural Test – a key requirement for claiming VGEC. We'll answer all your burning questions and show you how to maximise your claim to get the most out of this valuable tax credit.

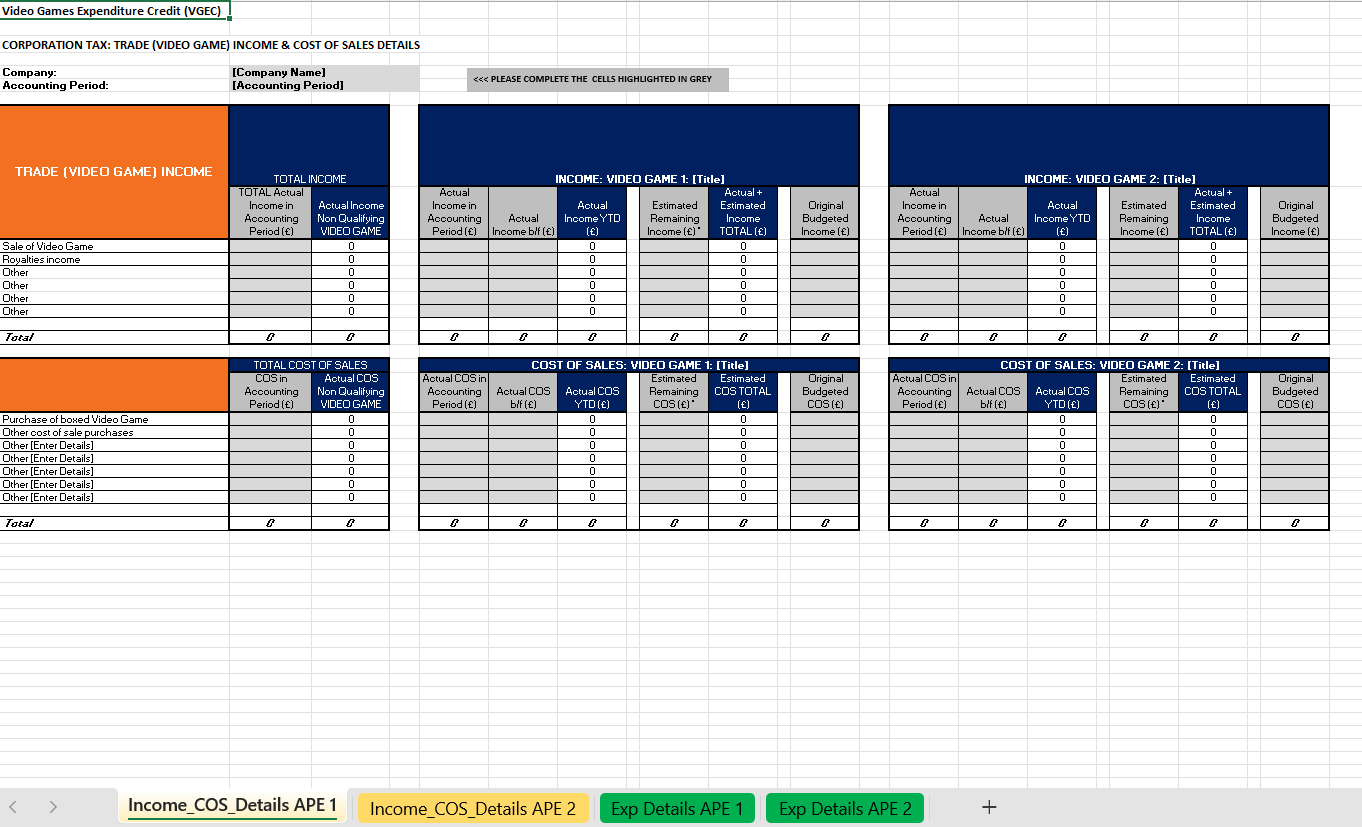

Simplify your Video Games Expenditure Credit (VGEC) claim with Myriad’s VGEC costing by trade spreadsheet, a powerful, structured template designed to help you satisfy both BFI and HMRC cost reporting requirements.

Key topics we covered include:

This free webinar explains how Special Purpose Vehicles (SPVs) can be used to structure video game productions in a way that avoids trapped losses and accelerates access to VGEC funding.

Myriad is your go-to partner for a successful Video Game Expenditure Credit claim.

Our experienced team of application specialists, cost accountants, corporate tax experts, and VGEC consultants have a reputation for helping UK game development companies unlock maximum value from government funding programs.

Let us help you claim VGEC for your project today!

If you want to claim VGEC, your video game must be certified as British. You must pass the British Film Institute (BFI) cultural test to receive this certification.

To pass the BFI cultural test, complete an online application form for each video game for which you want to claim VGEC. The BFI will assess your application and award points based on the cultural content of the game, its cultural contribution, its cultural hubs, and its cultural practitioners. Each video game must score at least 16 out of 31 points to pass the test. You’ll also need to submit some supporting evidence.

The certificate can be “interim” (for productions not yet completed) or “final” (for completed productions). An interim certificate is valid for three years and there is no limit on the number of interim certificates you can receive.

Myriad employs BFI application specialists who can help you pass this test. Contact us for advice.

BFI is currently reporting 10-12 weeks to process submitted applications.

Delays may occur if application forms are not correctly completed or need further information. If you need the certificate by a specific date, make sure you apply in good time and specify your deadline date on the application.

The Accountant's Report is required when an application claims points in Section C and/or Section D. The Accountant's report aims to verify the total and UK expenditure of the work in Section C and the nationality or residence of all persons in Section D.

The Accountant's Report must be prepared by a person eligible for appointment as a company auditor under section 1212 of the Companies Act 2006. A report can cost between £500 and £2,000 per application, depending on the video game costs and the number of applications you submit.

The BFI cultural test regulations require you to make a statutory declaration which states that the information you’ve given in your application is accurate. A statutory declaration is required for both the Interim and Final certifications.

The statutory declaration must be made before a practising solicitor, general notary, Justice of the Peace or an officer authorised by law to administer a statutory declaration under the Statutory Declaration Act 1835.

Some VGDCs may be carrying out research and development alongside their video game development.

A company can claim VGEC and R&D tax relief; however, the two schemes cannot be claimed on the same expenditure. Where VGEC is claimed on a specific cost, the VGDC can’t claim for any other reliefs (including R&D tax relief) for that cost. This means that if a VGDC chooses to claim VGEC, any research and development within the VGEC project wouldn’t qualify.

If a company can separate the R&D work from the video game development into separate projects with distinct expenditures, the two reliefs can be claimed within the same accounting period.

For example, developing an innovative game engine would be claimed under R&D tax relief, whilst developing a qualifying game would be claimed under VGEC. This would be true even if the game engine were used in the game's production, so long as no costs were claimed twice.

VGEC is not State Aid, which means that R&D ‘bubbles’ in video game projects are not precluded from receiving any of the R&D tax reliefs and/or expenditure credits. Your accounting period will determine the R&D tax relief scheme you can claim through.

The key to when core costs can be claimed is knowing when the project was “green-lit”. Initial concept design is usually undertaken to determine whether the video game is commercially feasible. Any expenditure in this stage is speculative in nature.

Once it is clear that the game development is going ahead, expenditure can be claimed. Some VGDCs may have very little conceptual development before proceeding with production, and some may spend more time assessing the commercial viability of a game.

Though game development may not always occur sequentially, claimants need to make an effort to split out conceptual development, production and post-production costs. You must identify which stage of development an item of expenditure contributes to, then determine how much is attributable to that stage.

Game and level designers may mostly be involved in conceptual development but may have some input at the development stages. Similarly, programmers and artists will be primarily involved at the production stage but may still be involved in pre- and post-production for feasibility analysis or debugging.

The game must not be intended for advertising, promotional or gambling purposes, nor can it contain any pornographic or extreme material.

The restriction on advertising or promotional purposes is designed to exclude games primarily created as advertisements or promotional tools. For instance, a free video game developed specifically to promote a film would not qualify for VGEC.

However, this restriction does not restrict games from supporting adverts or promotions within them. This is common, particularly for mobile apps with a free, ad-supported version alongside a paid, ad-free alternative.

The rule also does not disqualify games based on existing intellectual property. For example, a video game based on a television series would still be eligible as long as it was not produced solely to advertise the series but rather to capitalise on an established and popular franchise.

The gambling restriction is designed to prohibit games that allow players to win a prize that is money or worth money. If a video game includes mechanisms that enable players to “cash out”—whether earned through skill or chance—it is likely to be classified as gambling. This rule extends to cryptocurrencies and NFTs that can be traded or sold outside the game environment.

However, a game with elements that emulate gambling but do not allow players to win any real-world prize can be claimed. For example, a poker simulator that allows players to win in-game tokens will be eligible, so long as they cannot be cashed in.

HMRC has provided a non-exhaustive list of costs that cannot be included in a VGEC claim, largely because they do not contribute to the development of the video game:

Core expenditure must be apportioned on a “fair and reasonable basis". There are multiple ways you can define this, depending on the cost. You may wish to explain your methodology to HMRC to ensure you meet this criterion.

As with core and non-core expenditure, you will need to apportion UK and non-UK expenditure. Workers based in a UK office or working remotely in the UK can be included, but workers physically outside of the UK are ineligible. This applies regardless of where the company is based, the worker’s nationality or whether the company is in a group with the claimant.

For some costs that are partly based in the UK, you can choose how to apportion the cost. A staff member that works partly in the UK will only be eligible for the number of days they are working in the UK.

Some non-UK services are indirectly used in video games, such as services supplied by script/dialogue writers, concept artists, composers, and researchers. These are used by the developers and appear in the game having been transformed. HMRC will allow these costs to be included, although they will need to be apportioned based on where they are transformed. For example, suppose a German company provides concept art that is later used by a team of developers. In that case, it must be apportioned according to how many developers are in the UK.

With the arrival of the VGEC scheme, HMRC announced a transitional period to phase out the long-standing VGTR scheme without severely impacting any games currently claiming the existing relief.

For companies with accounting periods that cross over 1st January 2024 (i.e., the opening of the VGEC scheme), they will have the following options:

For companies with accounting periods that cross over the closure dates of the scheme (1st April 2025 or 1st April 2027, depending on the production timeline of the game, as above), they will have the following options:

Both VGTR and VGEC are cumulative schemes. Games that opt in for the VGEC scheme are treated as a continuation of the previous trade. In the same way, a BFI certificate will continue to be eligible under VGEC, even if it was acquired when claiming VGTR.

Some video game developers may be working on multiple games at once and they may have different preferences between VGTR and VGEC for each game. As each video game is treated as its own trade, companies can choose which scheme suits the game best on a per-game basis.

Companies may only opt into VGEC for accounting periods ending on or after 1st January 2024. They can only claim for expenditure incurred on or after this date, too.

However, for those still looking to claim the old VGTR scheme, the closure date depends on your game’s production timeline:

hello@myriadassociates.com

hello@myriadassociates.com